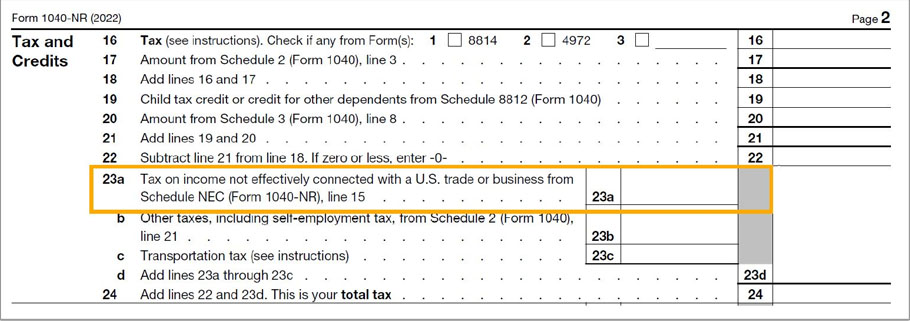

Capital Gains and Dividend IncomeCapital gains or losses for the sale of U.S. stocks may be subject to a 30% mandatory withholding rate or no withholding. This does not mean that this is the actual treaty rate. The sales and withholdings may be reported on Form 1099-B or Form 1042-S. Use the actual treaty to determine the proper rate. Start by referring to the table in Publication 4011. The sales are listed on Schedule NEC, with the applicable tax transferring to the Form 1040-NR, page 2. The sales are NOT listed directly on Form 1040-NR, page 1 for students. (These sales are not reported on Form 8849 nor Schedule D.) As students, U.S. stock sales are generally considered NOT effectively connected with the taxpayer's U.S. trade or business. Also, if the taxpayer was physically present in the U.S. for less than 183 days, the sales may be excludable under IRC §7701(b). Dividend income for the nonresident aliens is subject to 30% income tax rate, unless a lower rate is allowed by treaty. These lower treaty rates are Out of Scope for the VITA/TCE Foreign Student and Scholar program, as they are vastly different from one treaty to another and may contain several caveats. Due to their complexity, they should not be attempted to be interpreted for Foreign Student and Scholar VITA clients. The lower treaty rate countries are listed in Publication 4011 for reference, so that the volunteers will know which dividends may be permitted a lower treaty rate and need additional research. The taxable dividends are reported on Schedule NEC.

|

Tax Treaties

Tax Treaties

Table of income codes for aliens