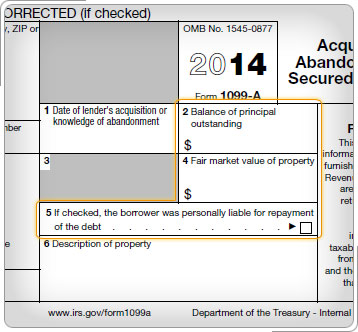

Form 1099-A (continued)Form 1099-A, issued by the lender, reports the outstanding debt and the fair market value of the property. This form provides information needed to determine the amount of any gain or loss due to foreclosure or abandonment. Report the gain or loss from Form 1099-A on Form 8949 and Schedule D. The sale price (amount realized) is based on whether the taxpayer is personally liable (recourse loan) or not personally liable (nonrecourse loan) for the debt.

Generally, if there is a loss on the sale of a principal residence or the entire gain is excluded under the Section 121 exclusion ($250,000 or $500,000 for Married Filing Jointly), the sale does not have to be reported. However, taxpayers who receive Form 1099-A should report the sale to account for the basis in the property. Failure to report the transaction on Form 8949 and Schedule D may result in an IRS notice to the taxpayer.

|