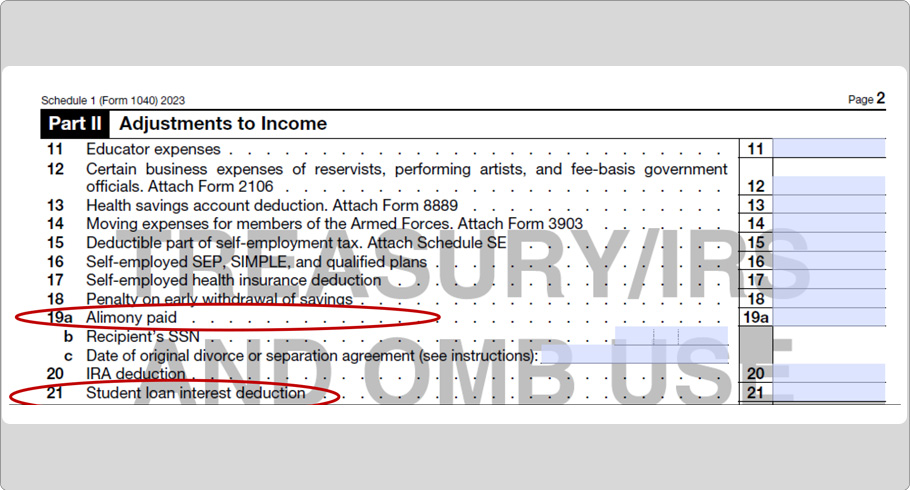

Adjustments to Income (continued)Student Loan Interest DeductionTaxpayers who paid interest on a student loan during the tax year may be able to deduct up to $2,500 of the interest paid. Taxpayers who paid $600 or more in interest to a single lender should have a statement from the lender showing the amount of interest paid. Alimony PaidTaxpayers who paid alimony to a resident of Puerto Rico during the tax year may deduct their eligible payments regardless of whether the recipient reports their income on a U.S. Income Tax return. Under the Tax Cuts and Jobs Act, alimony payments are no longer deductible by the payer and are not included as income to the recipient if the divorce or separation agreement was executed after December 31, 2018. Alimony payments made under a divorce or separation agreement executed before January 1, 2019, continue to be deductible by the payer and included as income to the recipient. Deductions that do not specifically apply to a particular type of income will be subject to the allocation required by Section 933. For more information and special instructions, see Publication 1321.

|